COVID-19 continues to have a significant impact on individuals and businesses and the insurance market has not escaped its impact. As the broader economy recovers and responds to the pandemic, the insurance industry faces a number of challenges but also see many new opportunities.

Impact of COVID-19 on the Insurance Market

“We all know that we are in the throes of a global pandemic that hasn’t been experienced in over a century and may never be experienced in many of our lifetimes again,” IBAC president and Wedgwood Commercial VP Kent Rowe wrote in a recently-released letter to IBAC members. “Like everyone, we’ve had to change the way that we conduct business in a pretty significant way.”

Not only have insurers had to adapt their process to a digital-first approach, but they’ve had to do so at a time when the property and casualty insurance market is hardening and clients need more communication, advice, and support than ever before. There’s a lot of change happening all at once.

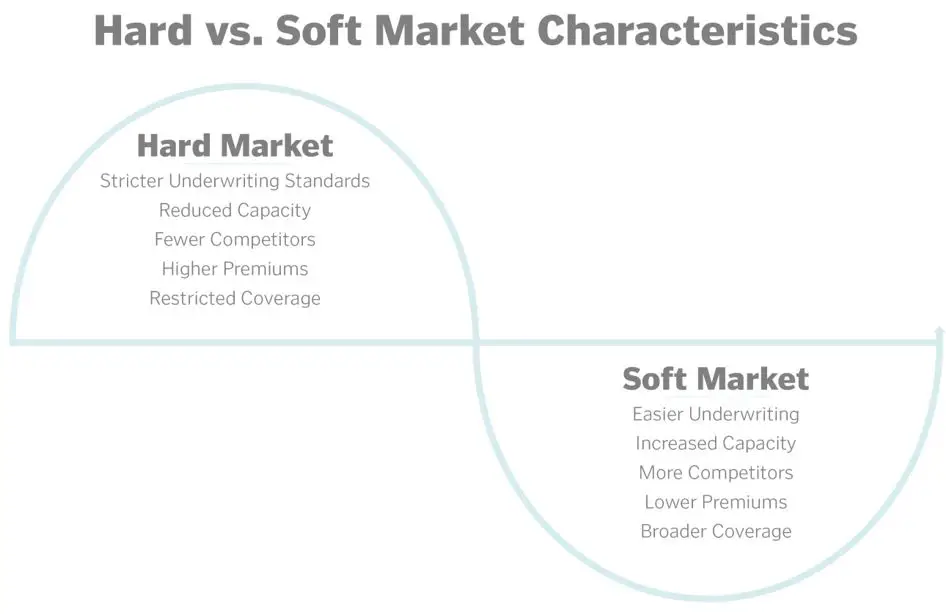

What is a Hard Market?

The insurance market is characterized by cycles. It fluctuates between soft market conditions and hard market conditions. Soft markets tend to be good for insurers because premiums hold steady or decrease. During a hard market, insurance rates increase and coverage is more difficult to obtain.

Most industries are cyclical to some extent, and insurance is no exception. As an insurance buyer, it’s important to know what factors determine the cost of coverage. But understanding the market cycle is only half of the pricing equation: since you can’t control the market, it’s equally important to know what you can do to ensure you are always securing the best price—whatever market conditions prevail.

Property-Casualty Insurance Cycle

The insurance industry pricing cycle alternates between periods of soft and hard market conditions. In a hard market, coverage is harder to place and premiums grow. A soft market indicates premiums are stable or falling, and insurance may be more readily available.

What affects the insurance market cycle? A variety of factors influence price, including economic downturns, catastrophic events, insurers’ claim reserve dollars, and supply and demand. Supply is tied to the amount of policyholder surplus in the industry, and demand is the appetite of the insurance-buying community to transfer risk.

Pricing cycles can also vary between lines of coverage and geographic location, creating both hard and soft market conditions depending on what type of commercial insurance is involved and how exposures to loss have changed. For example, the pricing and underwriting approach for property coverage for businesses based in hurricane-prone areas is much different than for businesses located elsewhere.

Risk Management Considerations

Industry experts have seen signs of hardening within the insurance market over the last year. Commercial insurance buyers should prepare for rising premiums and decreasing capacity from carriers in the coming year.

So, what should you do to ensure you are always getting the best price? Although premiums vary due to market pressure, your true cost of the price is determined by your claims history. The key to controlling price is to control losses through instituting safety prevention programs, managing claims efficiently when you have a loss, and employing cost containment strategies.

By working with an experienced Wedgwood Commercial Risk & Insurance Advisor, we’ll help paint your business in the best possible light to insurers. Continue to invest in your business to ensure your safety and loss control practices are best in class. Invest in repairs and maintenance on your fleet and property – if you own a building, invest in a sprinkler system for instance. Essentially you want to prove that you manage risks and hazards and don’t be afraid to boast about all of the great things you do to promote safety and manage/avoid losses.

In the 2011 P&C Insurance Coverages Survey sponsored by Zywave, Inc., 56% of respondents indicated that they considered themselves concerned or highly concerned about cost containment. If that describes you, we have the resources to help you employ cost reduction strategies to limit exposures and reduce premiums through both risk transfer and non-risk transfer solutions.

Our consultative approach includes:

- Identifying your exposures to loss

- Recommending loss control solutions

- Improving your disaster response potential by helping you to create or update a business contingency program

- Assisting in building a culture of safety

- Providing claims management to keep costs down

- Seeking continuous improvement

- Reviewing and recommending coverages to ensure your protection

Impact of the General Insurance Sector

According to a report from Deloitte, the pandemic has taken a toll on new premiums on certain lines of business, such as travel, events, and trade credit insurance, and losses from these lines of business may become significant. Other lines of business such as auto and home have remained relatively stable.

Claims volumes for personal lines (ie. auto) have greatly decreased due to the lockdown. This is not true from a business continuity coverage perspective as there has been a large volume of claims initiated.

How We Can Help

Navigating the COVID-19 crisis requires resilient leadership. Kent Rowe, in his President’s Message to IBAC members in May had this to say, “Winston Churchill once said ‘Never let a good crisis go to waste’, and I firmly believe that our industry is doing its best to make the most of our situation and to expedite and facilitate the necessary changes needed in our business that have been hanging over our heads for many years, if not decades.”

Those who approach risk financing through sustained long-term cost control and claims management measures, instead of just riding the insurance pricing cycle’s wave, are always in a better position to secure coverage at the best price.

COVID-19 may have caused the insurance market to fluctuate, but our goal has never wavered. To review your risk management strategies, contact us today.